Your House Went Up. Your Wealth Didn’t.

Real Estate Priced in Dollars vs. Bitcoin: Why the Most Popular Store of Value Is a Monetary Illusion

The Asset Everyone Calls a “Store of Value”

Ask any financial advisor, any parent, any banker what the safest long-term store of value is, and most will say real estate. It’s tangible. It’s leverageable. It’s been going up for decades. It is the foundation of the American wealth-building narrative: buy a house, build equity, retire comfortable. The problem is the measuring stick.

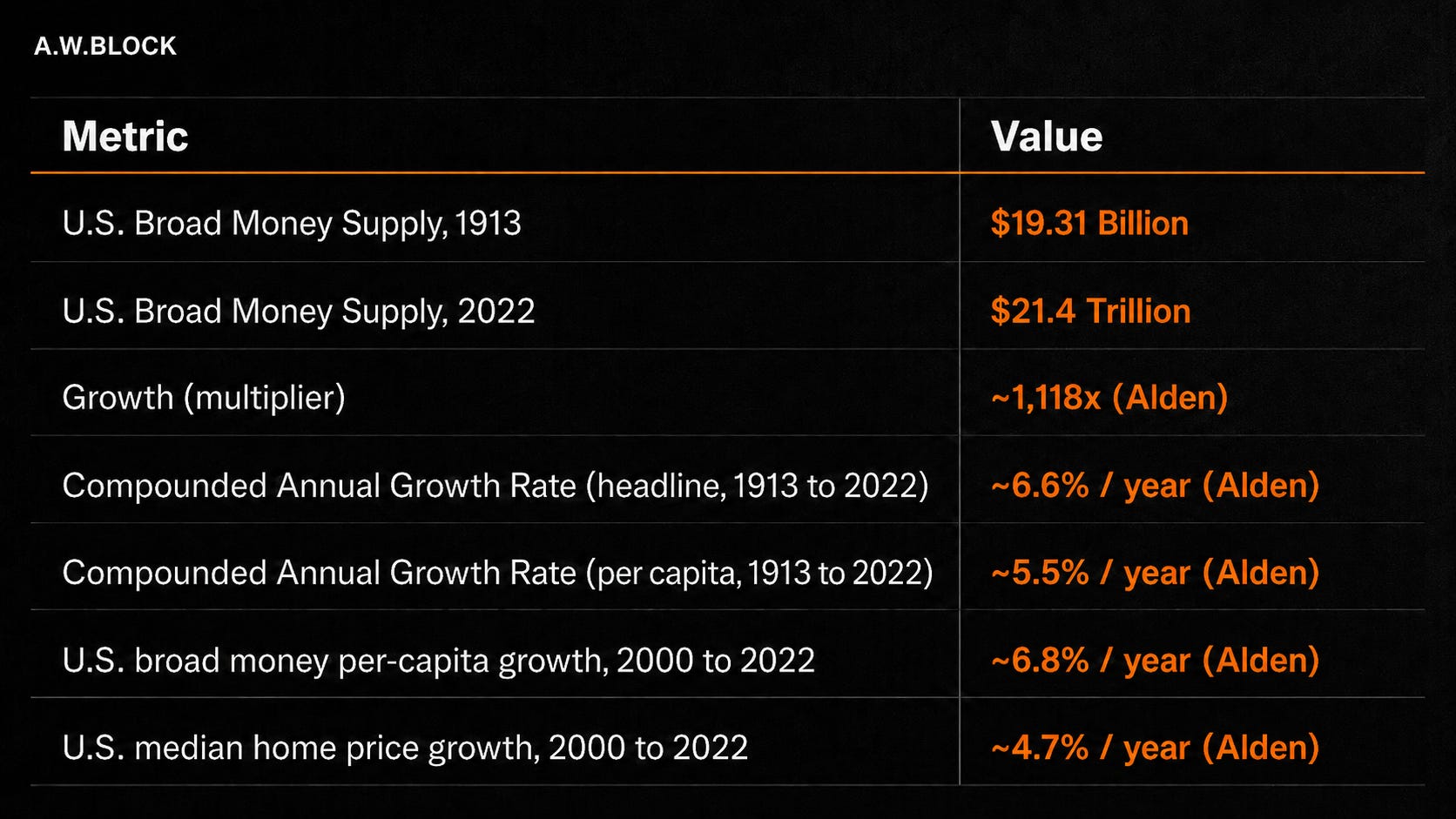

Real estate is priced in dollars. Dollars are not a neutral unit of measurement. Since 1913, when the Federal Reserve was created, U.S. broad money supply has grown from $19.31 billion to $21.4 trillion. That is a 1,118x increase, compounding at roughly 6.6% per year on the headline series, or 5.5% per year per capita (Alden, Broken Money). Every new dollar printed dilutes the purchasing power of every dollar already in existence. When the unit of measurement inflates, everything priced in it appears to go up. Most of the time, it has not.

The data above tells you almost everything you need to know. From 2000 to 2022, median home prices grew about 4.7% per year while per-capita money supply grew 6.8% per year. The house did not keep pace with the printer. It lost ground. The dollar number got bigger because the dollar got smaller, and it did not even get bigger fast enough to match the dilution.

The core claim of this document. Real estate priced in dollars looks like wealth creation. Real estate priced in a fixed-supply, non-dilutable asset reveals something different. The chart you have been looking at your whole life is not measuring what you think it is.

Real Estate Priced in Dollars

The chart below is the one everyone sees. U.S. median home prices from 2000 to 2025. Numbers go up and to the right. Most people stop the analysis here.

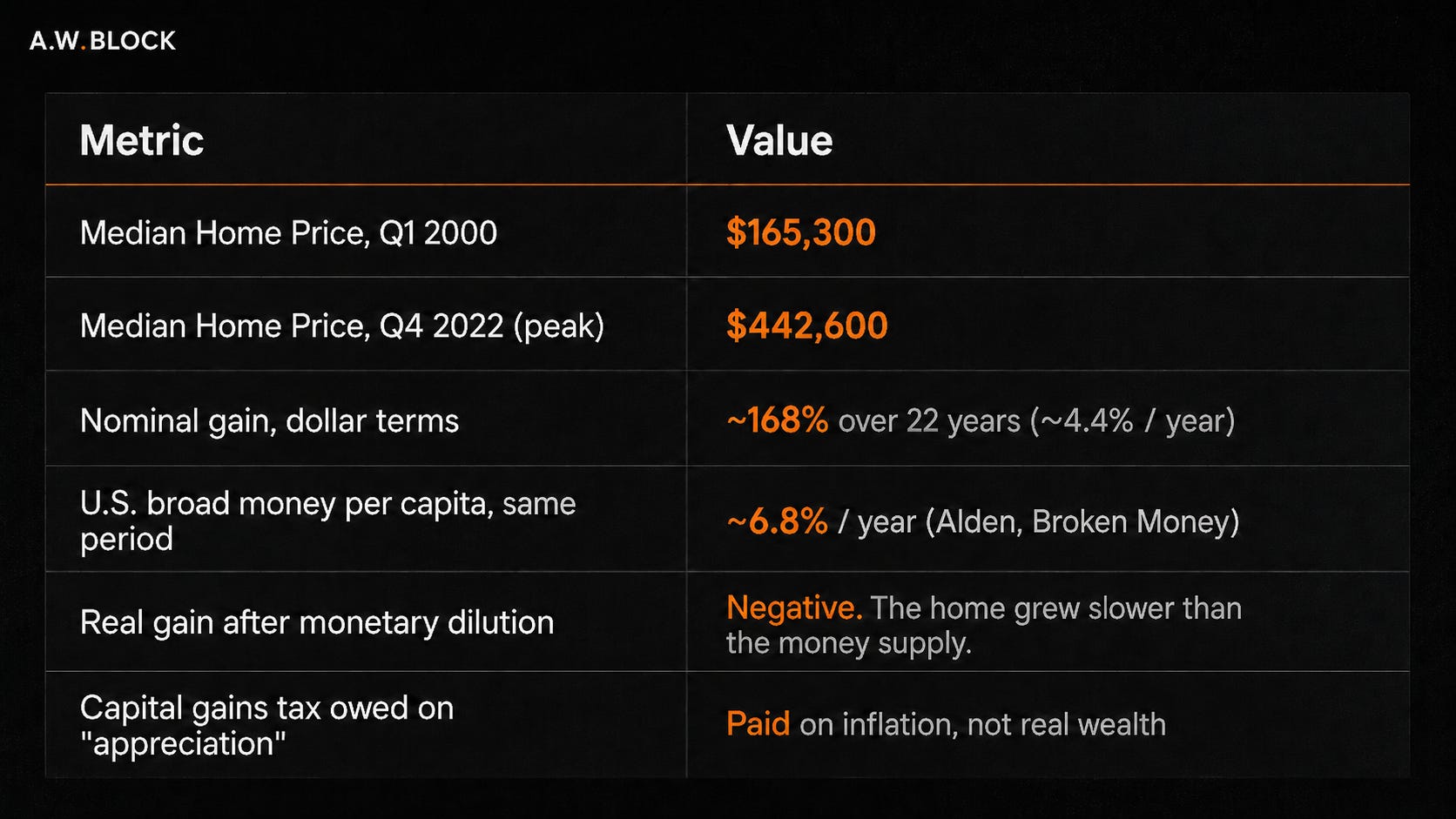

The median U.S. home rose from roughly $165,300 in Q1 2000 to a peak near $442,600 in Q4 2022, a 168% nominal gain over twenty-two years, or approximately 4.4% per year (Source: FRED MSPUS). On the surface, that appears to be a store of value. But measure that 4.4% gain against the per-capita broad money growth of roughly 6.8% per year over the same period (Alden, Broken Money). The house failed to keep pace with the printer.

Alden’s own figure for the median house price over 2000 to 2022 is 4.7% per year, in line with the FRED series. Both land near 4.5%, well below per-capita broad money growth of 6.8%. The dollar chart looks like appreciation. Against the money supply, it is a loss of ground.

You Pay Tax on Inflation

Lyn Alden illustrates the hidden cost precisely in Broken Money. Suppose you buy a $300,000 investment property. A decade later, with money supply growing at 2% per year, the property is worth roughly $365,000. The purchasing power of the house has not increased. It just kept pace with monetary dilution. But you still owe capital gains tax on that $65,000 increase, roughly $13,000 at a 20% rate. You were taxed on inflation. The government collected real revenue. You did not build real wealth.

Alden then runs the same example at 10% annual money supply growth. The $300,000 house is now worth $778,000 after a decade. The 20% capital gains tax on the $478,000 nominal “gain” is $96,000, which is 32% of the original house price. Purchasing power did not change. The state extracted nearly a third of the original property value through inflation alone. As Alden writes, “governments have an incentive to let inflation run hot, because thanks to capital gains taxes that are not adjusted for inflation or money supply dilution, they get a bigger share of transacted wealth if the dollar numbers are inflated.”

What the dollar chart hides. Maintenance costs. Property taxes. Transaction costs (5 to 6% each way). Debt interest. Insurance. The illiquidity premium. None of these appear in the price chart. Strip them out, and real estate as a savings vehicle performs far worse than the nominal line suggests.

Why Real Estate Became a Savings Vehicle

Real estate was not always treated as an investment asset. It was shelter, a consumer good. The transformation of housing into America’s primary savings vehicle was not organic. It was a direct consequence of broken money.

When Saving Becomes Impossible, People Buy Houses

Saifedean Ammous explains the mechanism in The Fiat Standard. When cash guarantees a loss, people flee into anything scarce. Stocks, gold, art, houses. Not because these assets are superior savings technologies, but because the alternative, holding dollars, is guaranteed wealth destruction. Real estate acquires a “monetary premium” far above its utility value as shelter, driven entirely by demand for something, anything, that holds value better than the currency.

“If bitcoin’s liquidity grows significantly, it would offer an increasingly compelling and efficient alternative to these technologies. Demand for these assets would become purely industrial and commercial rather than monetary. Housing would return to being thought of as a consumer good rather than a savings account or capital good. House prices would reflect demand for houses only as places to live, not as savings accounts.”

Saifedean Ammous, The Fiat Standard

The Consequences of Monetized Housing

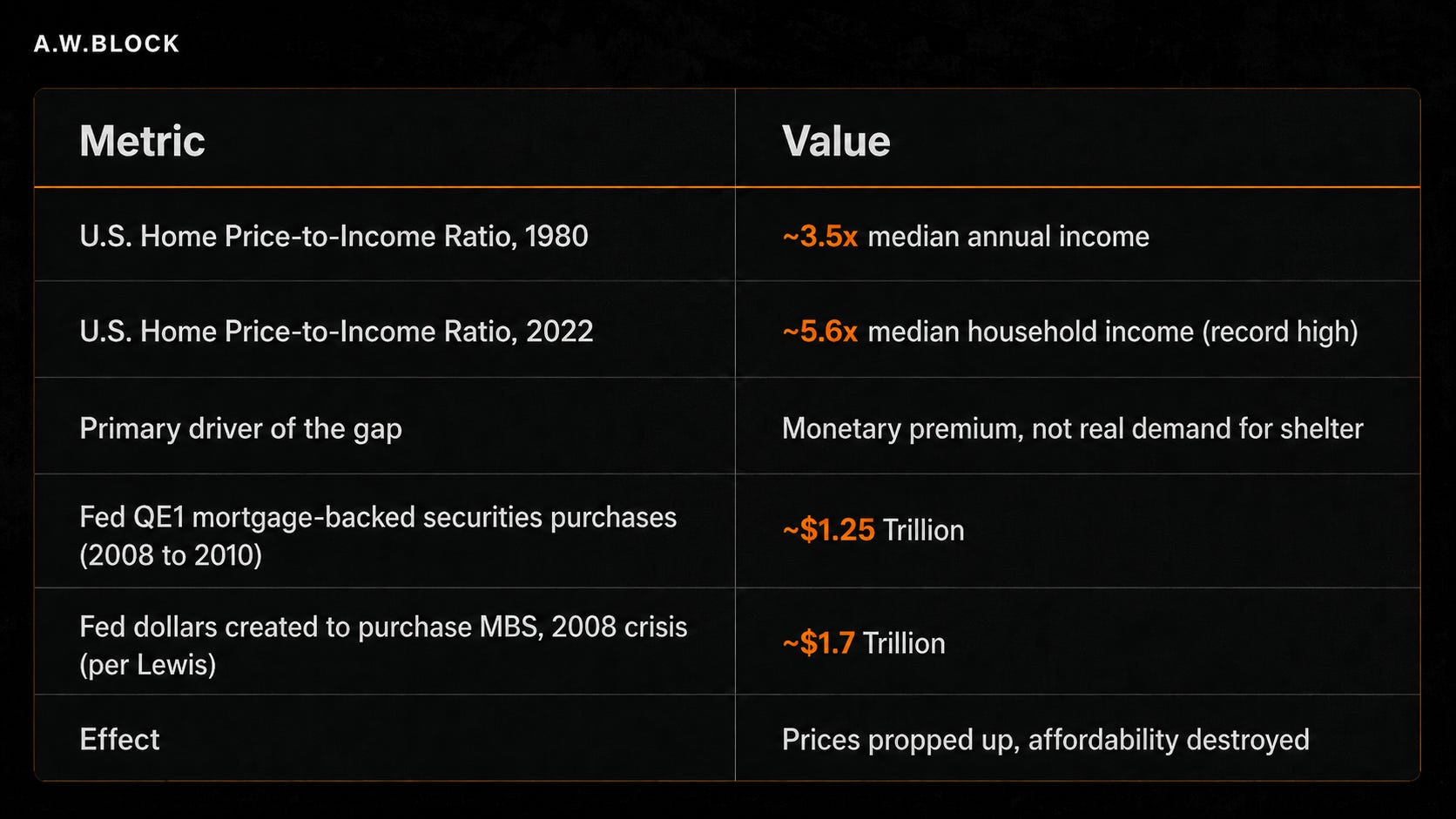

When housing becomes a savings vehicle, the consequences are predictable and severe. Lyn Alden documents the dynamic in Broken Money. Wealthy investors and upper-middle-class buyers purchase second and third homes with cheap credit, crowding out first-time buyers. The ratio of home prices to incomes climbs to levels that make homeownership structurally difficult for younger generations without high debt loads. Global capital flight amplifies the problem. Wealthy individuals escaping currency instability in their home countries park money in desirable real estate markets, pushing prices further beyond the reach of local earners.

The hidden social cost of fiat money is not just diluted savings. It redirects capital into non-productive uses, artificially inflates the cost of shelter, and creates periodic housing crises when the monetary premium eventually collapses.

Parker Lewis describes the policy response in Gradually, Then Suddenly. During the 2008 crisis, Lewis writes, “the Fed increased the supply of dollars to ‘stabilize’ the dollar value of real estate.” He continues that, just as falling prices would have made homes more affordable, “the Fed stepped in to increase the price of real estate, specifically housing, making it that much more expensive and further out of reach.”

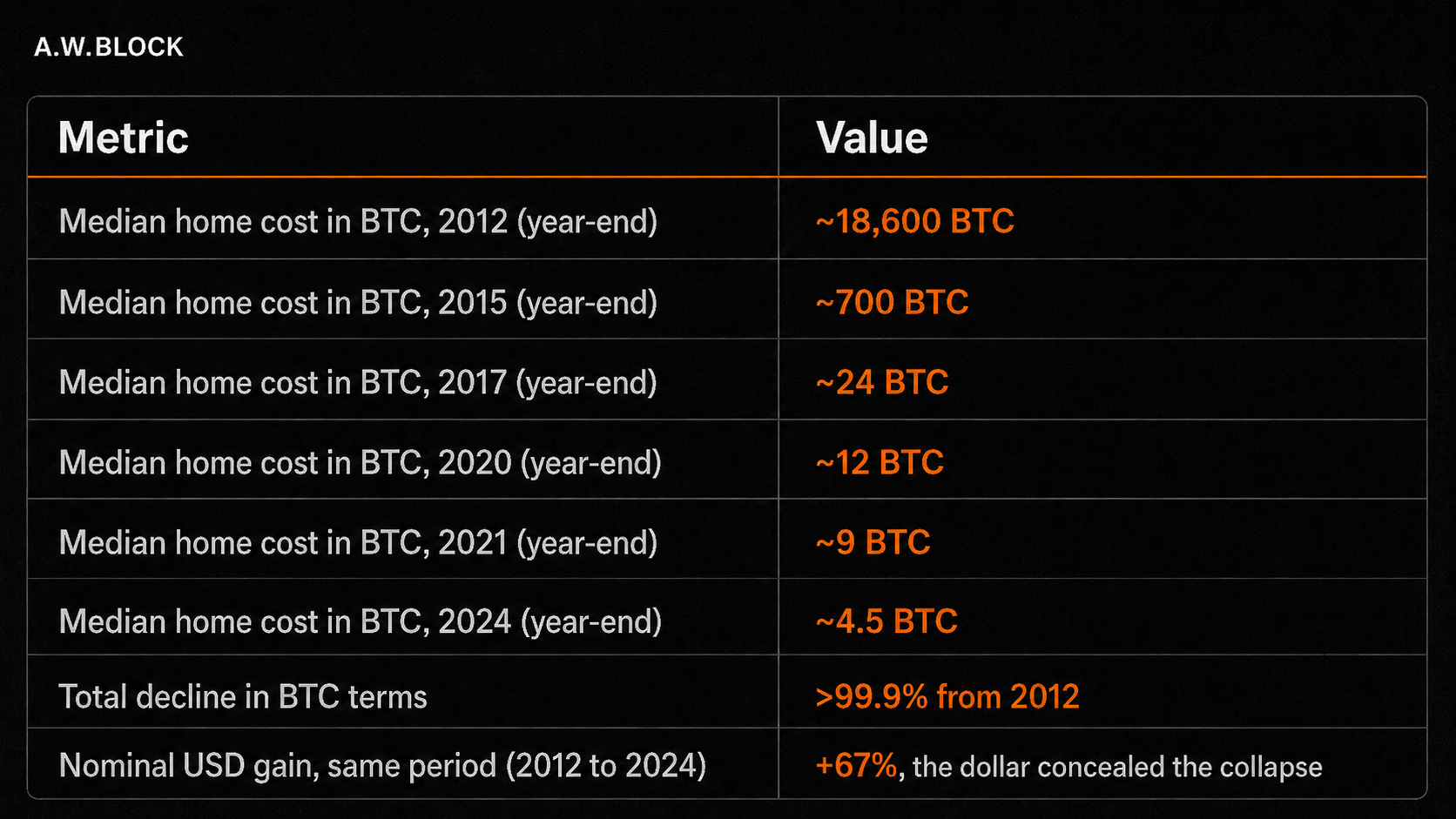

Real Estate Priced in Bitcoin

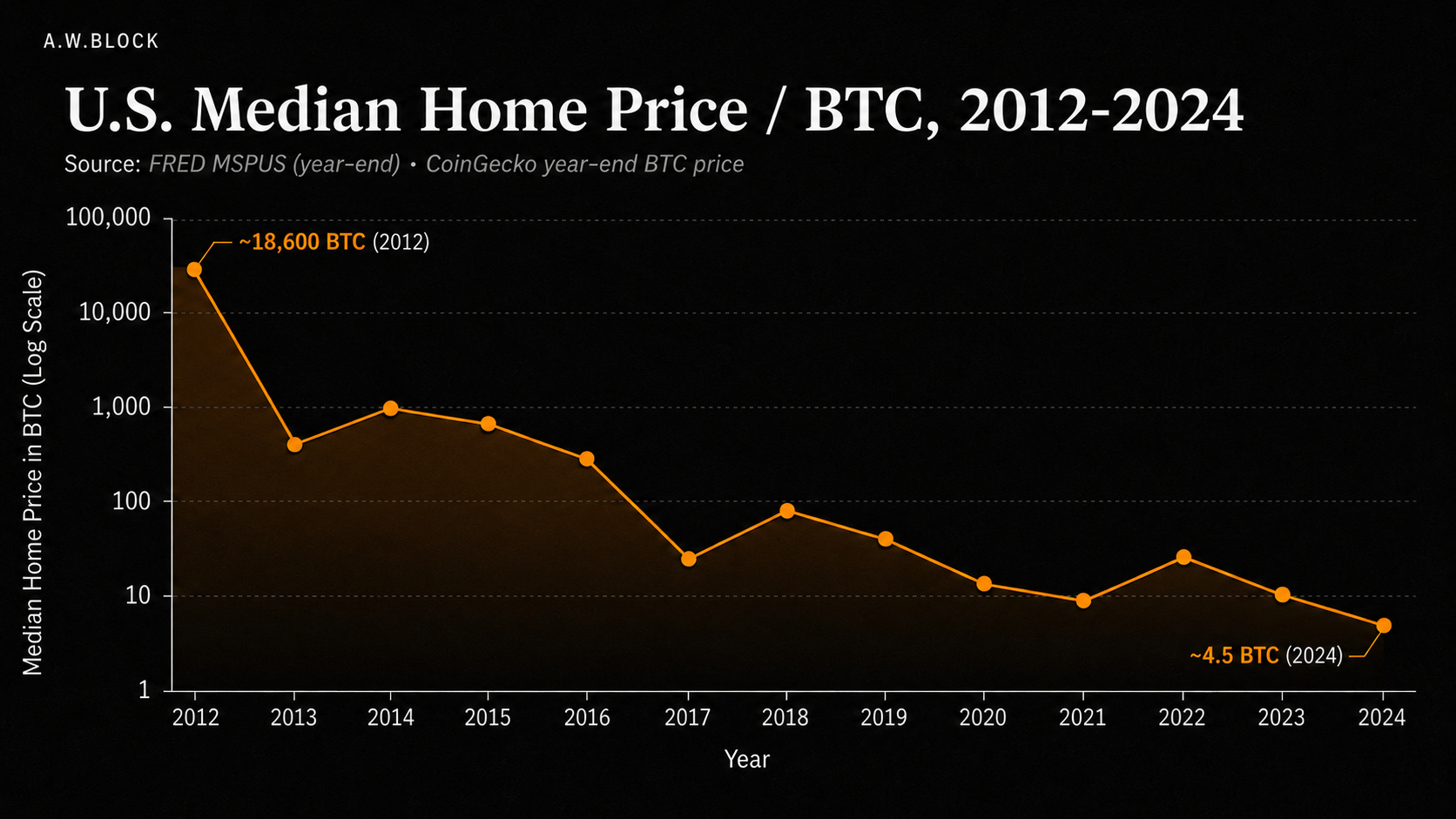

Now change the measuring stick. Instead of pricing real estate in a currency that can be printed without limit, price it in Bitcoin, a fixed-supply asset capped at 21 million units forever. This chart tells the true story.

Note on chart methodology: Median home price is the Q4 (year-end) FRED MSPUS value for each year. BTC reference price is the December 31 closing price per CoinGecko. Different conventions (annual mean, annual high, monthly close) will produce different ratios.

In 2012, when year-end BTC was ~$13.50 and the year-end median U.S. home was ~$251,700, the median home cost roughly 18,600 Bitcoin. By 2024, with year-end BTC at ~$93,400 and the median home at ~$419,300, that same median home cost roughly 4.5 Bitcoin. Real estate has lost over 99.9% of its value measured in Bitcoin over that period. Over the same twelve years, the dollar price of that home rose about 67%. Both numbers measure the same asset. One is using a shrinking ruler. One is not.

Why This Happens, and Why It Will Continue

Bitcoin has a fixed supply of 21 million. No central bank. No monetary policy. No mechanism by which supply can be expanded in response to demand, political pressure, or crisis. Every four years, the rate of new Bitcoin issuance is cut in half through the halving. The terminal inflation rate of Bitcoin approaches zero, fully issued by approximately 2140. The dollar has a stated 2% annual inflation target, meaning policymakers intend to perpetually dilute it, and has historically grown at 6 to 7% per year in broad money terms.

When you price a fixed asset (a house) against a fixed-supply currency (Bitcoin), you see the trajectory of the asset itself. When you price it against an inflating currency (the dollar), you see a distortion driven primarily by the unit of measurement.

“Bitcoin is becoming the scarcest form of money that has ever existed. Finite scarcity is a property no other form of money has ever or will ever achieve.”

Parker Lewis, Gradually, Then Suddenly

What You Should Walk Away With

Real estate priced in dollars appears to appreciate. It has not, in real terms. From 2000 to 2022, median home prices grew about 4.7% per year while per-capita money supply grew 6.8% per year. The house lost ground to the monetary base. The nominal gains are real in dollar terms. The real gains in purchasing power are negative over the long run.

You are taxed on inflation. Capital gains tax applies to the full nominal appreciation of your home, regardless of whether that appreciation reflects real wealth creation or monetary dilution. Alden’s own examples show the state can extract 30% or more of the original property value through inflation alone at elevated money-supply growth rates.

Real estate became a savings vehicle because money is broken. Housing is not naturally an investment. It is shelter. The monetary premium in home prices exists because holding dollars guarantees loss. Remove that premium, and home prices reflect only the utility of shelter.

Priced in Bitcoin, real estate has lost over 99.9% of its value since 2012. The dollar made your house look like a winning investment. Bitcoin shows how much purchasing power the asset lost relative to a scarce reference.

The right question is not “Did my home go up?” It is “Up relative to what?” Dollar terms flatter. Bitcoin terms clarify.

Sources: Broken Money (Lyn Alden) • The Fiat Standard (Saifedean Ammous) • Gradually, Then Suddenly (Parker Lewis)

Data: U.S. Census Bureau / FRED (MSPUS) • CoinGecko • Harvard Joint Center for Housing Studies

About A.W. Block

A.W. Block is a Pennsylvania-based Bitcoin advisory firm founded by William Sanchez Jr. The firm provides Bitcoin self-sovereign advisory, digital asset estate and probate consulting, and expert witness services for legal professionals navigating blockchain-based assets. Every engagement is designed to leave clients needing A.W. Block less.

This document is for educational purposes only. It does not constitute financial, investment, or legal advice. All data references are sourced from publicly available research, cited texts, and generated charts based on U.S. Census Bureau, FRED, and CoinGecko data. Past performance of any asset does not guarantee future results. Consult a licensed financial advisor before making any investment decisions.

awblock.io | @awblockbitcoin