The Market Is Up. Your Wealth Might Not Be.

Why Measuring Stock Performance in Dollars Is the Wrong Question, and What Bitcoin Reveals

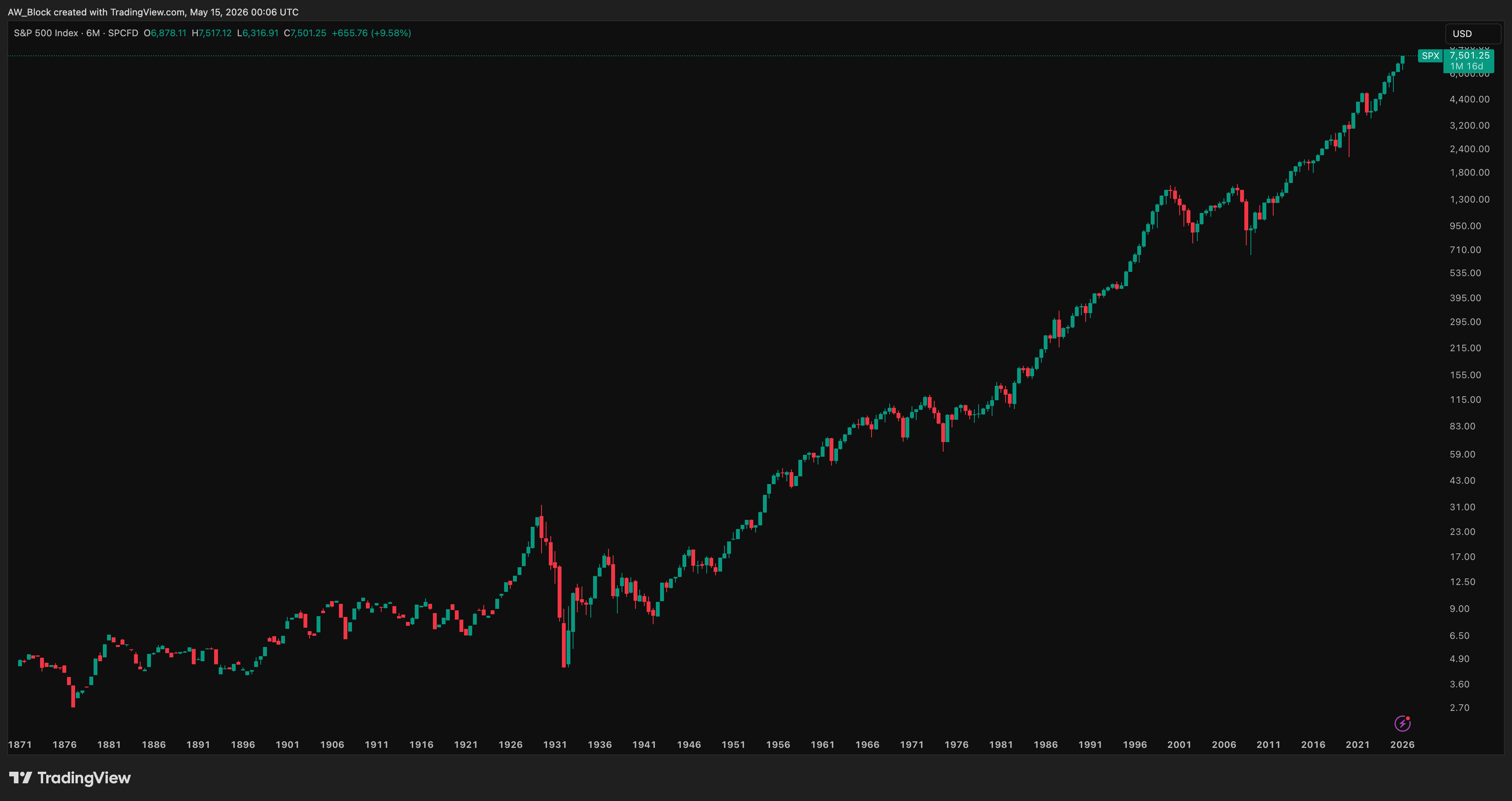

The S&P 500 in Dollars

The chart below shows the S&P 500 Index priced in U.S. dollars from the late 1800s through today. At first glance, it looks like a story of uninterrupted wealth creation. The index sits near 7,100, up from single digits a century ago. Most investors look at this chart and feel good. That feeling is a measurement error.

The dollar you are using to measure that growth is not a constant. It is a shrinking ruler. Between 1913, when the Federal Reserve was created, and 2022, U.S. broad money supply grew from $19.31 billion to $21.4 trillion. That is an increase of 1,118 times, compounding at approximately 6.6% per year on the headline series and 5.5% per year on a per-capita basis. The per-capita figure went from roughly $199 per person in 1913 to over $64,800 per person in 2022, a 325-fold increase (Alden, Broken Money).

The core problem. When you measure growth in dollars, you are measuring it against a unit that central banks can, and do, expand without limit. The chart going up does not tell you whether you are gaining real wealth. It tells you the price changed. Those are different things.

Section 02 - The Shrinking Ruler Problem

M2 Money Supply: The Number Nobody Shows You

From 1971, the year Nixon closed the gold window, to today, U.S. M2 money supply has grown from approximately $632 billion to over $22 trillion (Source: Federal Reserve Economic Data, M2SL series). That is an average annual growth rate of roughly 6.7% over fifty-four years. Every dollar that enters the system dilutes the purchasing power of every dollar already in it. This is not a bug. It is how the system is designed.

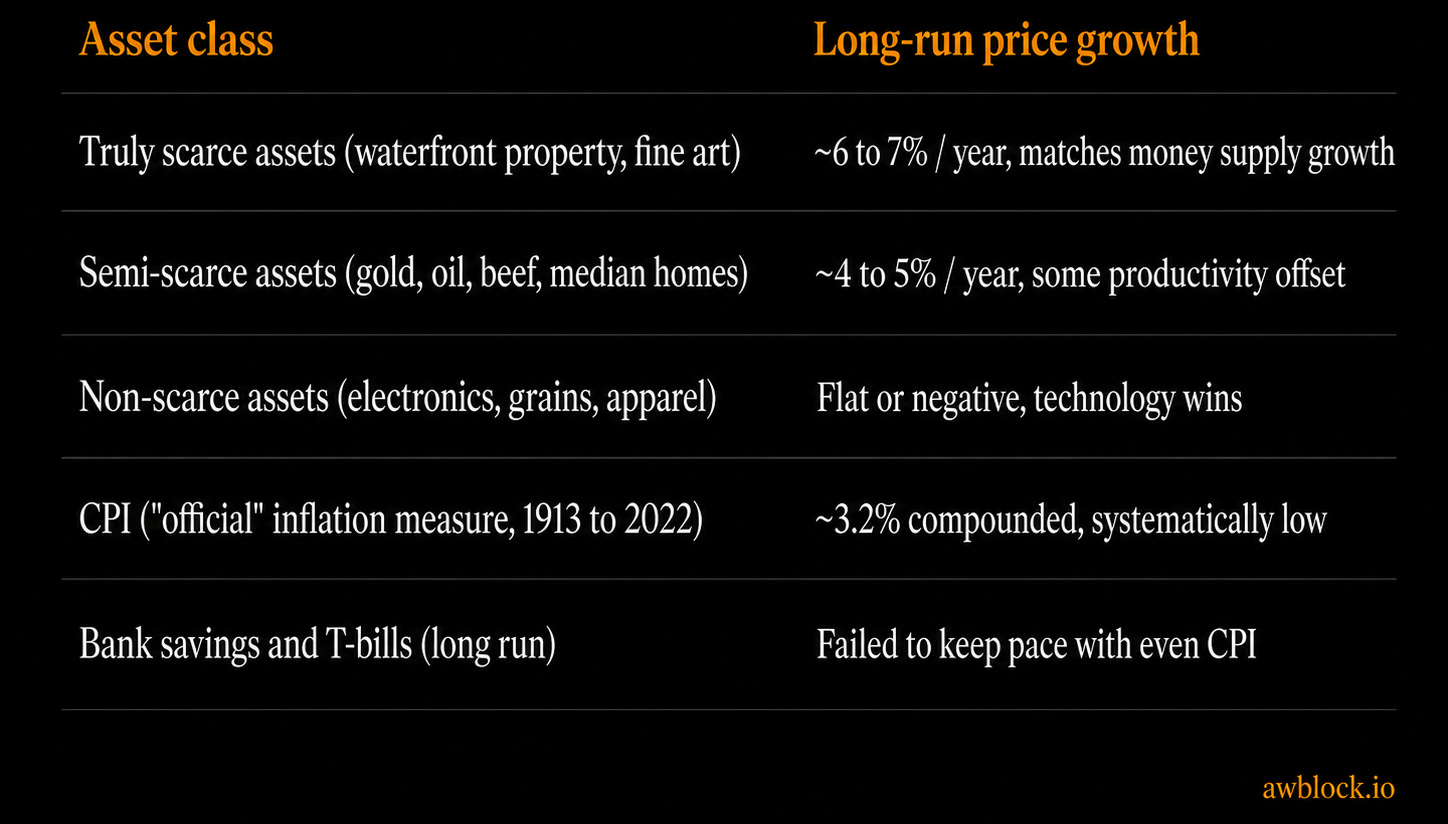

What Actually Inflates, and by How Much

Not all assets inflate equally. Lyn Alden’s framework from Broken Money is the clearest way to understand this. The numbers below reflect Alden’s documented 2000 to 2022 series, where broad money per capita grew at 6.8% per year:

Alden states the rule directly:

“If the assets that you are saving in are not going up in price at the growth rate of broad money supply per capita over a long stretch of time, then your purchasing power is being diluted.”

— Lyn Alden, Broken Money

CPI: The Faulty Yardstick

Most people accept CPI, the Consumer Price Index, as the official measure of inflation. It is published by the Bureau of Labor Statistics and cited in every financial media outlet. It is also structurally broken as a unit of measurement.

The Three Core Problems with CPI

1. The basket changes with prices. As the dollar loses value and prices rise, people cannot afford the same goods. They substitute cheaper alternatives. The basket adjusts downward in quality, and CPI records near-zero inflation. The ribeye becomes a soy burger. The measure does not capture your actual decline in living standard.

2. It has no fixed unit. Ammous notes in The Fiat Standard that CPI attempts to measure the change in value of the dollar by using the dollar itself as the ruler. He writes that this is, “to a large degree, a mathematical tautology and an infinite referential loop.” There is no independent, constant reference point. Time has seconds. Weight has grams. CPI has nothing.

3. Key costs are deliberately excluded. Home prices, the single largest consumer expense, were removed from the CPI basket under the argument that a house is an “investment.” Food and energy are routinely stripped from “core” CPI. Economist Stephen Roach, who began his career at the Fed in the 1970s and is cited in Ammous, The Fiat Standard, has said then-chairman Arthur Burns fought inflation by removing rising-price items from the basket entirely. Roach states Burns eliminated about 65% of the goods in the CPI, including food, oil, and energy-related products.

Inflation Is a Vector, Not a Number

Michael Saylor’s key insight, presented in Breedlove’s What Is Money? series, Episode 9, and incorporated by Ammous in The Fiat Standard: inflation cannot be summarized in a single number. It is a vector. It moves differently for different people depending on what they own, where they live, and what they spend their income on. A retiree spending heavily on healthcare, housing, and insurance faces a real cost-of-living increase well above the headline CPI rate. A tech worker buying laptops and streaming subscriptions sees deflation in their key categories. CPI averages across both, and tells neither the truth.

“Persistent inflation of the money supply allows policymakers and various middlemen to siphon off the purchasing power of peoples’ savings without them being able to easily keep track of it.”

— Lyn Alden, Broken Money

The conclusion. When you see the S&P 500 up 9% in a year and CPI at 3%, the headlines say you gained 6% real return. But if money supply per capita grew 6 to 7% that year, and your actual cost of living in housing, healthcare, and education grew 6 to 9%, the real picture is flat to negative. You worked, you invested, and you stood still.

Financialization: The Forced Bet

There is a reason the average American is expected to own stocks, bonds, ETFs, and real estate. It is not because investing is inherently rational for everyone. It is because holding cash guarantees you lose. This forced participation in financial markets is called financialization, and it is a direct consequence of monetary debasement.

How Soft Money Creates a Risk Mandate

Parker Lewis, in Gradually, Then Suddenly, points out that a 2% annual inflation target produces roughly a 20% loss in purchasing power over a decade and 35% over two decades. Every person in that system is not choosing to invest. They are being compelled to in order to avoid guaranteed loss. Lewis describes the dynamic directly: the Fed created a problem, and then a treatment for the problem was necessary. Financial products emerged that would not otherwise exist. People are pushed to take risk to replace what monetary inflation strips away.

You Have to Earn Your Money Twice

Ammous frames the absurdity precisely in The Fiat Standard: in a hard money world, a doctor, engineer, or accountant who earns money and saves it retains wealth. In a fiat world, that same professional must now also develop expertise in portfolio allocation, risk management, equity valuation, global macro trends, and real estate cycles, or hire someone who has. Ammous puts it plainly: under fiat, you need to earn your money twice. Once when you work for it, and again when you invest it to beat inflation. The investment management industry exists largely to help people defend their savings against the very monetary system that threatens those savings.

Stocks are up because money is weak. That is not the same as saying the economy is strong or that your wealth is growing. Large equities acquire a “monetary premium.” Investors flee cash and pile into equities not because the underlying businesses justify the valuation, but because equities are a better store of value than the dollar. Strip out the monetary premium, and much of the stock market’s nominal gains evaporate.

Alden frames the same dynamic this way: when money in a society keeps degrading in value, there is a strong incentive to hold other things that have greater scarcity, and thus to add a monetary premium to those other things above and beyond the utility value of those things (Broken Money).

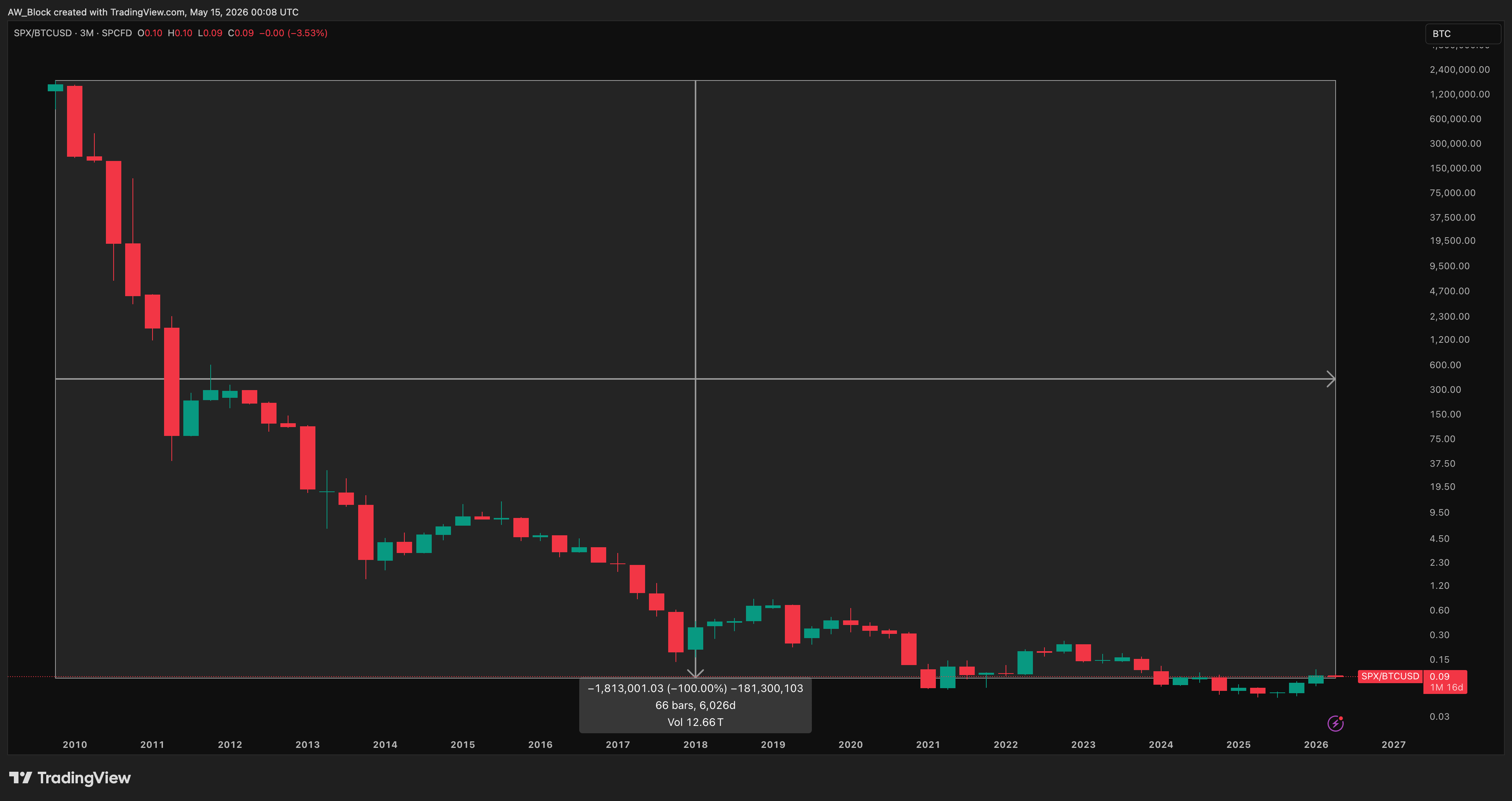

The S&P 500 Priced in Bitcoin

Now look at the same stock market, but measured in Bitcoin instead of dollars. The chart below shows SPX/BTCUSD on a 3-month timeframe beginning around 2012. The story it tells is radically different.

In the early 2010 period, when Bitcoin traded in the low single digits, it took several hundred Bitcoin to buy one unit of SPX value. Today, that same unit of S&P 500 value costs approximately 0.09 Bitcoin. The S&P 500 has lost over 99% of its value relative to Bitcoin over this period. The dollar made the market look like it went up. Bitcoin reveals that it went down badly.

What you are seeing. Bitcoin is not going up because it is speculative. The S&P 500 is going down when measured against a scarce asset. The chart in Section 01 is nominal. This chart is closer to real. Your retirement account may be worth more dollars. It may be worth far fewer Bitcoin.

Why Bitcoin Is a Better Measuring Stick

The Supply Cannot Be Changed

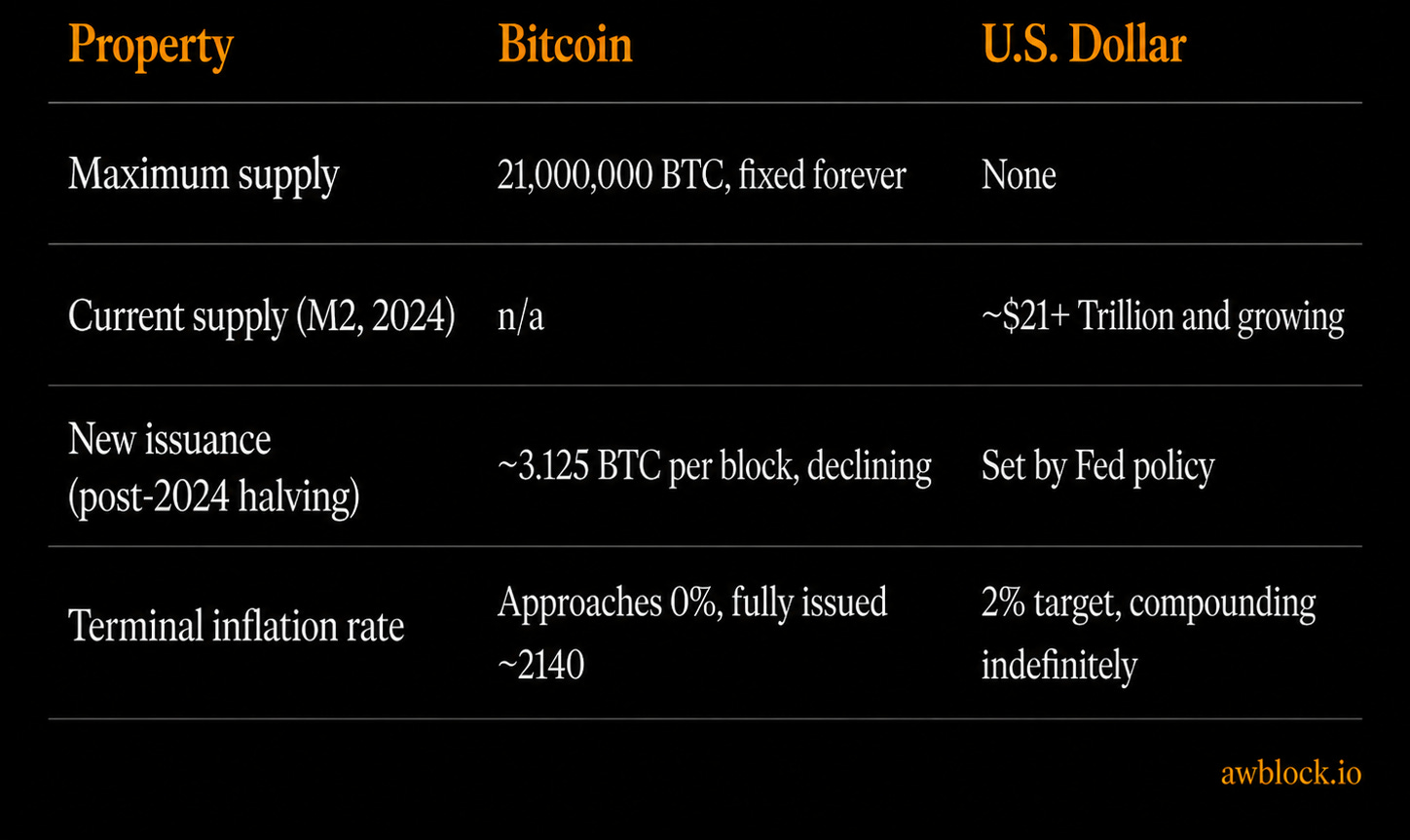

The property that makes Bitcoin a legitimate unit of measurement for wealth is the one thing no other monetary asset has ever achieved: absolute, enforced, fixed supply. There will only ever be 21 million Bitcoin. This is not a promise. It is a protocol enforced by a decentralized network of nodes operating independently, with no central authority capable of altering it. No CEO. No Fed chair. No act of Congress.

Scarcity Is What Makes a Measuring Stick Work

To measure something accurately, your ruler must be constant. A ruler that shrinks invalidates every measurement taken with it. The dollar shrinks. Bitcoin does not. Parker Lewis summarizes the point directly in Gradually, Then Suddenly:

“Bitcoin is becoming the scarcest form of money that has ever existed. Finite scarcity is a property no other form of money has ever or will ever achieve.”

— Parker Lewis, Gradually, Then Suddenly

Lewis frames the asset’s core property: holding Bitcoin represents an immutable right to own a fixed percentage of all the world’s money indefinitely. Every other monetary asset, gold included, has some mechanism by which supply can expand. Bitcoin does not.

This Doesn’t Mean Dump Your Portfolio

This analysis is not investment advice. It is a diagnostic. The goal is not to tell you to liquidate equities. It is to help you understand what your portfolio is being measured against, and whether that measurement is giving you an accurate picture of your wealth. If your benchmark is the dollar, you may be winning a rigged game. If your benchmark is a scarce, fixed-supply asset, the picture looks different.

The Definancialization Thesis

If monetary debasement created the current era of financialization, the forced investment of savings into risk assets, then sound money would logically reverse it. This is what Parker Lewis calls the Great Definancialization.

In a hard money world, someone who accumulates savings does not need to actively manage a portfolio to maintain wealth. Savings hold value by default. The incentive to speculate in leveraged instruments, chase yield in bond markets, or pile into equities at inflated multiples diminishes because the base money is working. The current system forces everyone to become an investor just to preserve what they already earned.

The Side-by-Side Reality

“What if all that was ever really needed was just a better form of money? Suppose each individual had access to a form of money that was not programmed to lose value. Rather than taking perpetual and open-ended risk, everyone could get back to saving.”

— Parker Lewis, Gradually, Then Suddenly

The Takeaway for Stock Market Investors

You have been trained to ask, “Is my portfolio up this year?” The better question is, “Up relative to what?” Relative to the dollar, a unit that loses 5 to 7% of its supply-adjusted value annually, you may appear to be doing well. Relative to a scarce, fixed-supply asset, you may be running in place.

This is not an argument against equities. It is an argument for intellectual honesty about the unit of account you are using. Measuring wealth in an inflating currency is measuring distance with a shrinking ruler. You can do it. Just understand what the number means.

What You Should Walk Away With

The dollar is not a neutral measuring stick. It loses supply-adjusted value at roughly 5 to 7% per year. Any asset measured in dollars will appear to grow even if its real purchasing power stands still.

CPI understates true inflation. The basket changes with prices, key costs are excluded, and it has no fixed unit. It is a politically managed metric.

The S&P 500’s long-term dollar gains are partly real, partly monetary illusion. Strip out money supply growth and the compounding dilution of the dollar, and the real gains are considerably more modest.

Priced in Bitcoin, the S&P 500 has lost over 99% of its value since 2012. This does not mean Bitcoin is perfect. It means the contrast reveals something important. Bitcoin’s fixed supply makes it a more stable measuring stick for wealth over time.

Financialization is a symptom, not a feature. Forcing everyone to take investment risk just to preserve savings is a consequence of broken money, not evidence of a healthy economy.

The right question is not “Is my portfolio up?” It is “Up relative to what?” Change your benchmark and you may find a different answer.

Sources: Broken Money (Lyn Alden) • The Fiat Standard (Saifedean Ammous) • Gradually, Then Suddenly (Parker Lewis) • What Is Money? Saylor Series (Robert Breedlove)

About A.W. Block

A.W. Block is a Pennsylvania-based Bitcoin advisory firm founded by William Sanchez Jr. The firm provides Bitcoin self-sovereign advisory, digital asset estate and probate consulting, and expert witness services for legal professionals navigating blockchain-based assets. Every engagement is designed to leave clients needing A.W. Block less.

This document is for educational purposes only. It does not constitute financial, investment, or legal advice. All data references are sourced from publicly available research, cited texts, and TradingView charts. Past performance of any asset does not guarantee future results. Consult a licensed financial advisor before making investment decisions.

awblock.io | @awblockbitcoin